Core US Inflation – The Highest Two-Months Increase in Three Decades

The US inflation data for the month of May was released last week. The data came out at the same time as the European Central Bank started its monetary policy meeting last Thursday.

Because the two events were the main events of the trading week, the markets did not move in the prior days. In fact, the ranges on most of the FX pairs were so tight that one may have argued that summer trading conditions are already here.

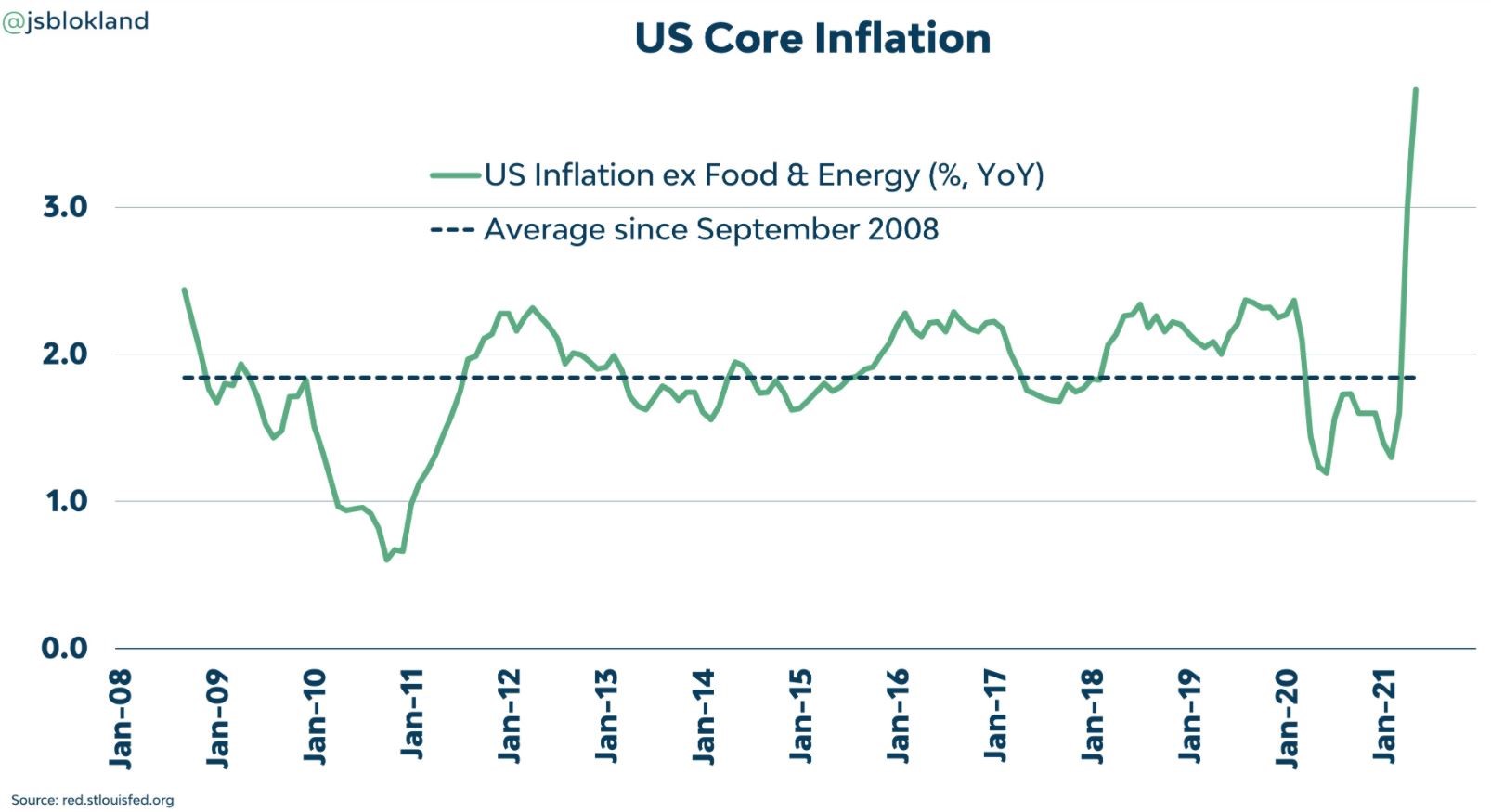

When the Consumer Price Index (CPI) was released, it showed that the prices of goods and services in May were increasing much faster than expected. As always, the CPI comes in two versions – the headline report and the core report. The latter is the one that matters for the Fed because it is not considering the food and energy prices – too volatile to be included in the report.

The headline CPI data for the month of May was expected to increase by 0.4% – it came out at 0.6% on a month-over-month basis. Also, the core data was expected at 0.5% – it came out at 0.7%.

With both headline and the core CPI beating expectations by a mile, coupled with the inflation data for the previous months, we see the highest two-month increase in inflation in three decades.

{kind=link}

What About the Fed?

The Federal Reserve of the United States (Fed) has a dual mandate. To create jobs and to maintain price stability.

Naturally, inflation refers to the price stability part of the Fed’s mandate, and this one changed during the pandemic. More precisely, the Fed shifted its inflation mandate last August, from targeting 2% to averaging 2%. Out of the two releases, the Fed focuses on the core CPI.

Yet, the Fed did not mention so far what is period it considers when averaging inflation. The longer the period, the more it will allow inflation to rise.

At the start of the 1970s, as inflation escalated, then US President Nixon abandoned the Bretton Woods system, shocking financial markets and the international community. At the end of that decade, the Fed’s Chair, Paul Volcker, introduced bold anti-inflationary measures because inflation exceeded 13% on an annualized basis.

Last week’s data means that the core CPI reached 3.8% in the United States on an annualized basis. Central banks like the Fed argue that this is transitory and that the prices will cool down eventually.

While there is a long way to 13%, no one is expecting the Fed to raise the rates as Volker did back in 1979. Instead, all the Fed should do is to signal the tapering of its asset purchases. That might do the trick to stop the upside pressures on the prices of goods and services, and the Fed has the chance to do so this week, at its Wednesday meeting.