Decisive Week for Monetary Policy - Will the Fed Turn to Negative Interest Rate Policy

Busy week ahead for investors and traders alike, as major central bank interest rate announcements are due. In a world dominated by the health crisis and its negative economic impact, traders turn to central banks for guidance about how to cope with the downturn.

Bank of Japan to Start the Week

Bank of Japan (BOJ) is the first one in line to announce its monetary policy decision. Nikkei reports that the BOJ wants to transform the current Quantitative Easing (Q.E.) program into an unlimited one, with implications on USD bonds due to new Japanese inflows. The JPY traded sideways lately, and this coming week has the potential to break the recent ranges.

The coronavirus crisis already created unprecedented unemployment levels around the world. It far exceeded the 2008 Great Financial Crisis in terms of the economic damage and policy-decision makers barely cope with the situation. The problem does not seem to be a recession anymore, but most likely a depression ahead.

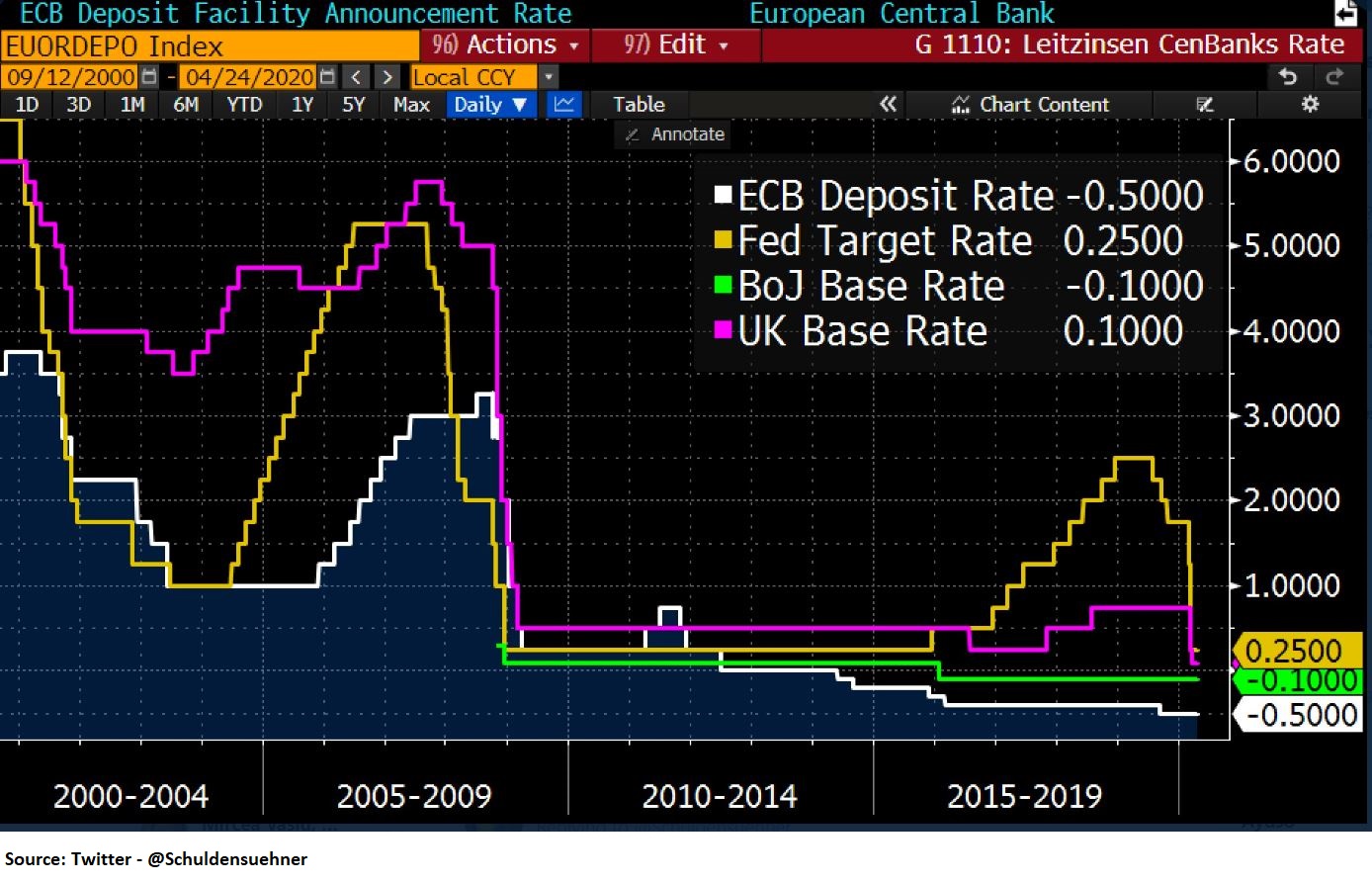

Is the Fed Going Negative?

Besides BOJ, the other two main central banks are due to deliver their monetary policy statements on Wednesday and Thursday – the European Central Bank (ECB) and the Federal Reserve of the United States (Fed). Out of the three, only the Fed still has a positive interest rate policy, but many voices started to argue that negative interest rates are close to being introduced in the United States.

{kind=link}

In fact, the former President of the Fed Bank of Minneapolis, Kocherlakota, says that the Fed should go negative next week – to fight a deepening recession, it should take U.S. interest rates below zero for the first time ever. Such a move is not priced in the markets and most likely will send the USD much lower. Even if the Fed does not turn the policy negative, the dovish tone should dominate Wednesday’s announcement, only normal after the United States saw over twenty million unemployment claims in the last five weeks alone.

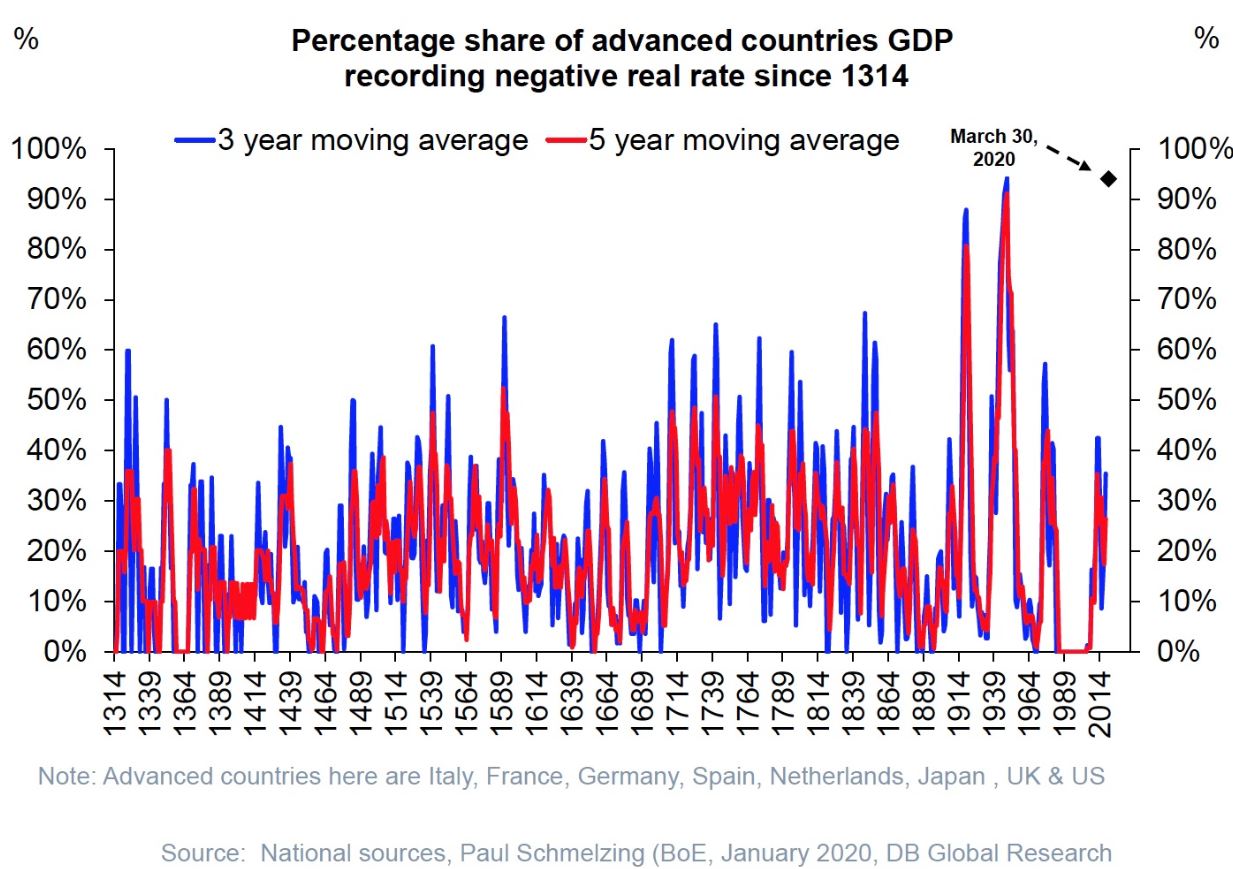

Negative interest rates have long failed to impress markets anymore, but the Fed kept saying they are not an option in the United States. Given the unprecedented scale of the current crisis and the percentage share of advanced countries GDP recording negative real rates, any hint that the Fed might follow the same path should not be that surprising.

{kind=link}

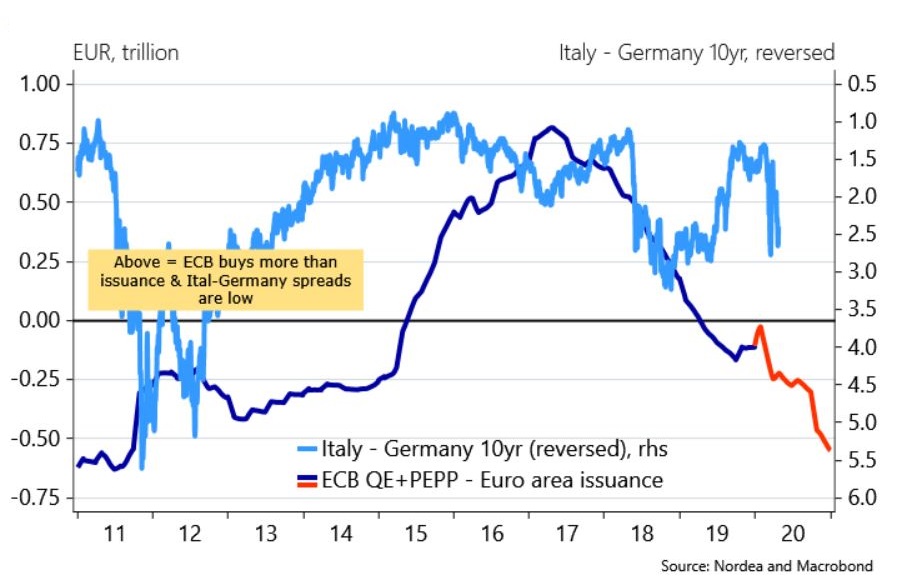

Debt-Sharing Still an Issue in the Euro Zone Area

Last to join the central banks’ statements this week is the ECB. The Euro area PMI’s last week revealed that the current crisis is far deeper than the GFC, and the Euro suffered from policy-makers indecision. More and more voices call for the introduction of the Eurobonds, but Nordic voices still oppose debt sharing concepts. The Euro traded with a bearish tone all last week up until Friday when it recovered a bit of the lost ground.

On Thursday, the ECB might announce an increase in its bond-buying program to the relief of spread markets. Compared to the Fed, the ECB is not buying it all, as the Fed does, so it should come as no surprise if it announces a step-up of its bond-buying program.

{kind=link}

Conclusion

Expect a wild week ahead with increased volatility. With the U.S. equity markets already recovering a big part of the initial losses caused by the coronavirus crisis, look for this week’s central banks’ announcements to pave the road for the entire second quarter and beyond.