Dovish Message From the Fed Sent Markets Lower

Last Wednesday, the Federal Reserve of the United States (FED) delivered its FOMC Statement and economic projections for the period ahead. Despite no initial reaction, the equity markets in the United States sold aggressively towards the end of the week, with the Dow Jones Industrial Average (DJIA) ending the week over two-thousand points lower since the Fed’s announcement.

{kind=link}

Accommodative Stance to Continue

The Fed’s projections showed the accommodative stance to continue well into the future. More precisely, the Fed members saw the federal funds rate remaining at current levels for as long as the projections go – 2022.

As a reminder, despite the fact that the FED is not a central bank that actively targets inflation, it recognized that price stability is one part of its mandate. Moreover, it considers the 2% inflation rate as the level at which inflation is not too low to threaten a move below zero, and not too high for money to lose value. Price stability, therefore, is maintained when inflation sits at the symmetrical 2% target.

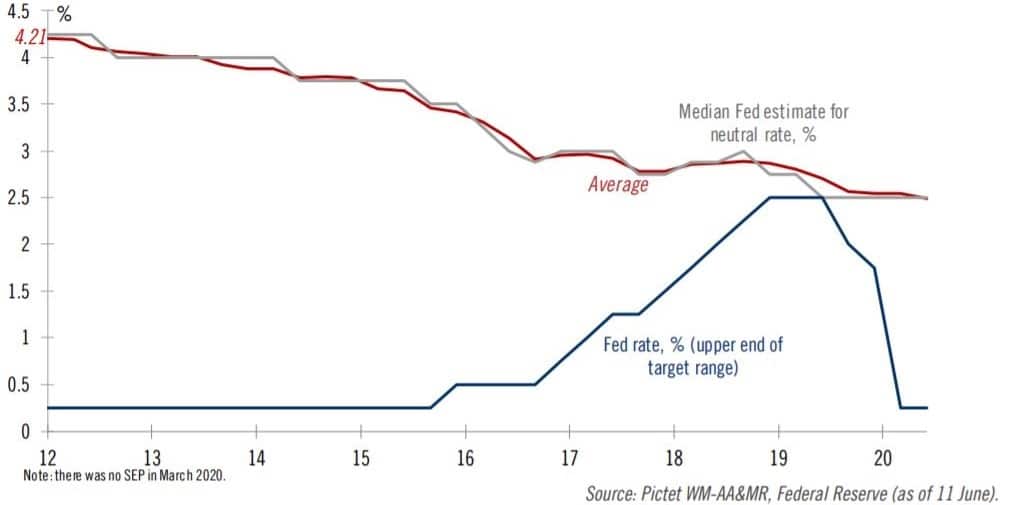

The benchmark for the official rate set by any central bank of a developed economy is the neutral rate. When the official rate is below the neutral rate, it is said that the monetary policy is accommodative (adjusted by the economic growth rate). Conversely, a contractionary monetary policy has higher official rate when compared with the neutral rate and economic growth.

The Fed tightening cycle that started with Janet Yellen sent the funds rate close to the neutral rate. And then the pandemic started.

While the Fed remains accommodative, the equity markets took its projections as dovish. The Fed projects the unemployment rate to fall back to 5% in a couple of years, but there is little or no evidence that this is the case.

One day after the Fed’s message, the initial jobless claims and the continuing claims disappointed again. Moreover, they spell troubles for the encouraging NFP May numbers, fueling the suspicion that the NFP data had errors.

Coupled with a record surge in US crude oil inventories, the data triggered a selloff in US equity markets. All major indices declined, while the USD rose across the board – except against the JPY and CHF, viewed as safe-haven currencies.

During the coronavirus pandemic, the US equities turned out to be of significant importance as most risk assets correlated with the rise and fall in equities. Therefore, the dovish message from the Fed had repercussions on all financial markets, particularly on the currency market.

The focus shifts now to how the pandemic evolves. As more states in the US open up, the chances for a second wave of infections increase. If that is the case, the Fed, as well as the Congress, will act again.

Will we see negative interest rates in the United States soon?