Negative Oil Price Shock Keeps Haunting Economic Recovery

The coronavirus pandemic shocked the financial world in ways no one thought possible. Fiscal and monetary policy stimulus from governments and central banks helped ease the economic pain, but everyone agrees more is needed on the medium and long term.

The economic crisis that unfolded exceeds a mere contraction. It even goes beyond recessionary concepts and into economic depression. More precisely – long-lasting economic recession with negative consequences on the medium to long-term economic growth.

Only in the United States, 38 million people lost their jobs in the last nine weeks. If we use the number as a benchmark for the developed world, other economies suffered similarly high unemployment rates.

On top of high unemployment and lockdown economies, the price of oil delivered another blow. Economic growth spurs demand for oil, so the price of oil acts as a bellwether for economic performance. The coronavirus disruption of oil demand led to the price of oil turning negative.

{kind=link}

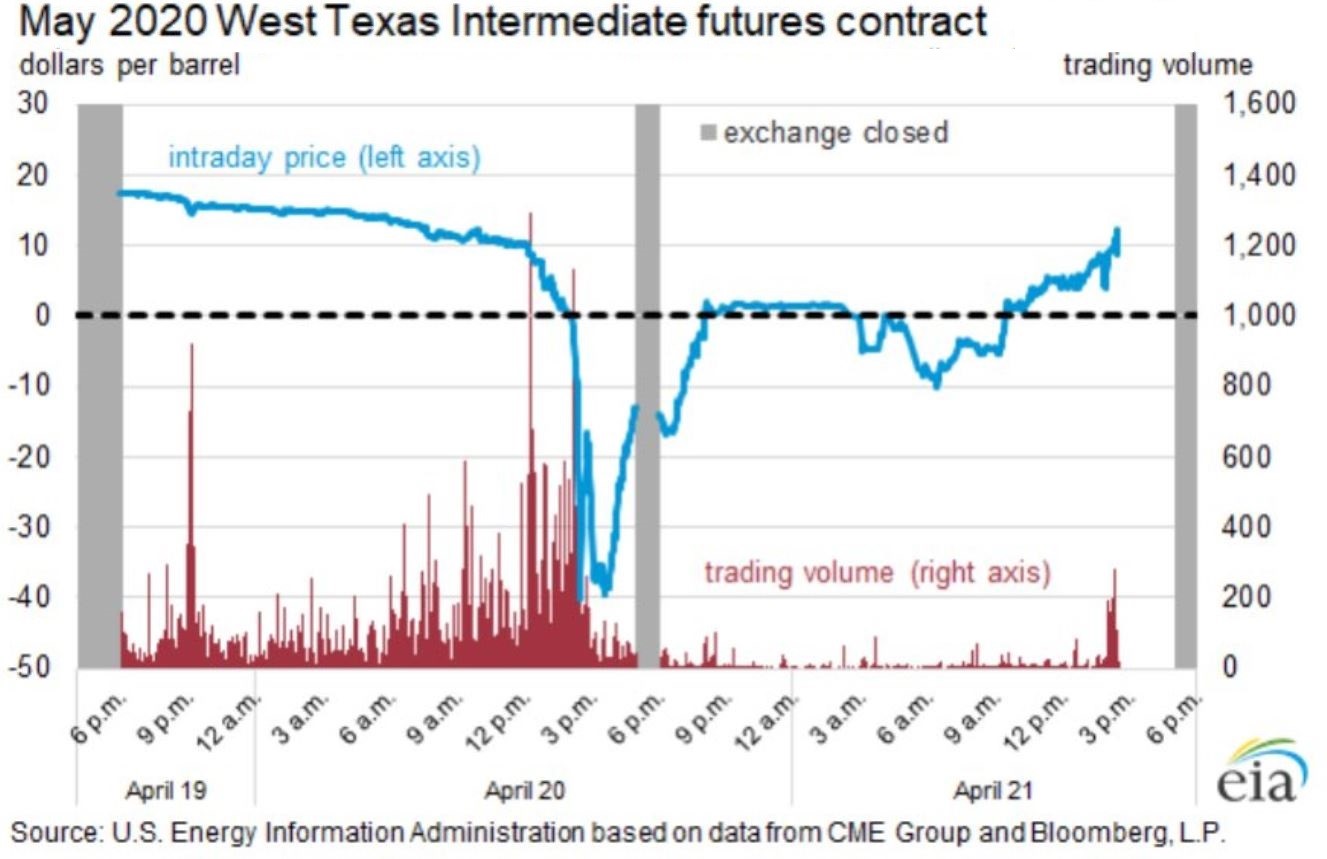

A month ago, the price for the oil futures contract dropped below zero. A futures contract is a derivative – a contract that settles daily and the clearinghouse debits or credits each party account with the gain, respectively the loss, depending on how the price of oil moved during the trading day.

In April, there were no bids for the oil futures contracts. Effectively, it means it was no buyer. As such, the price kept falling until it settled for the day at almost -$40/barrel.

The oil industry suffered some shocks throughout its history, but nothing compared with what happened this April. The event was quickly dubbed “Black April” as producers effectively paid for someone to come and take the oil from their hands – no storage was available.

The price of oil recovered in the meantime, as China opened up, and other economies gradually plan to do so too. However, negative oil prices set a dangerous precedent not only for the oil industry but for financial markets too.

First, the clearinghouses (in the case of the WTI contract that went negative, the clearinghouse was the CME) now know that they can list negative prices. Up to this April, such a possibility was not even considered.

Second, even if the price of oil bounced, the second-round effects in terms of low inflation and possible deflation will force central banks to further ease the monetary policy (if possible) and/or to extend the current easy policy for much longer than initially thought.

{kind=link}

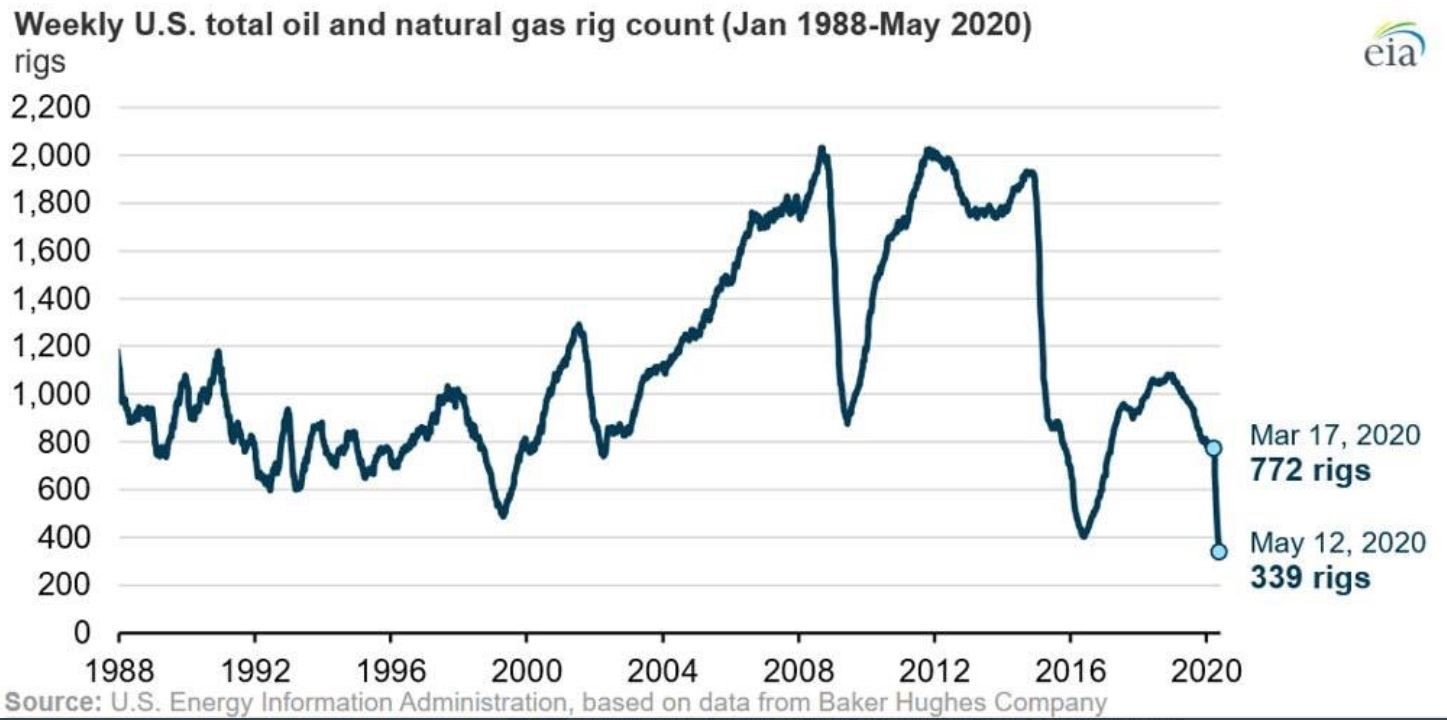

Finally, the decline in oil prices was first caused by a disagreement between Russia and Saudi Arabia to cut production levels. The aim was to hurt the US shale oil industry, as the US became a net exporter of oil for the first time in many decades.

The pandemic, though, sent the prices much lower than anyone had anticipated. Yes, it hurt and still hurts the US shale industry, as the oil rig count continues to drop to this day.

But it also hurt Russia, Saudi Arabia, OPEC, and the general economic conditions, because without stable oil prices, central banks have a hard time fulfilling their price stability mandate.