Strong Demand for Dollars Continues

The USD surged across the board since the coronavirus pandemic outbreak with no sign that things will change anytime soon. Why is it that investors prefer the USD, even though all the Fed actions lately are designed to weaken it? The answer comes from how the monetary policy transmission mechanism works and from the key role of the USD in the international financial system.

Before the current health crisis, the Fed just finished a tightening cycle. It delivered three rate cuts as mid-cycle adjustment, as it reached its mandate of price stability and 2% inflation.

Meanwhile, the rest of the developed world was near the zero level with the interest rates. At one point, the United States had the highest interest rate in the developed world. Naturally, the demand for USD surged, as Bank of Japan or the European Central Bank had (still have) negative interest rates.

The health crisis caught everyone by surprise. From central banks to governments, from emerging to developing economies – everyone turned to safety. In the world’s financial markets, safety equates the USD.

The Fed quickly slashed the funds rate to zero in an emergency meeting. Still, the dollar surged as investors looked for safety. After all, even at zero, the federal funds rate is still higher than negative as in other parts of the world. Moreover, the Fed signaled that it does not consider negative rates, so the bids for the USD continued. This last weekend the newly appointed Governor of Bank of England said that the institution considers negative rates. Therefore, forward guidance keeps suggesting the bid for the USD remains.

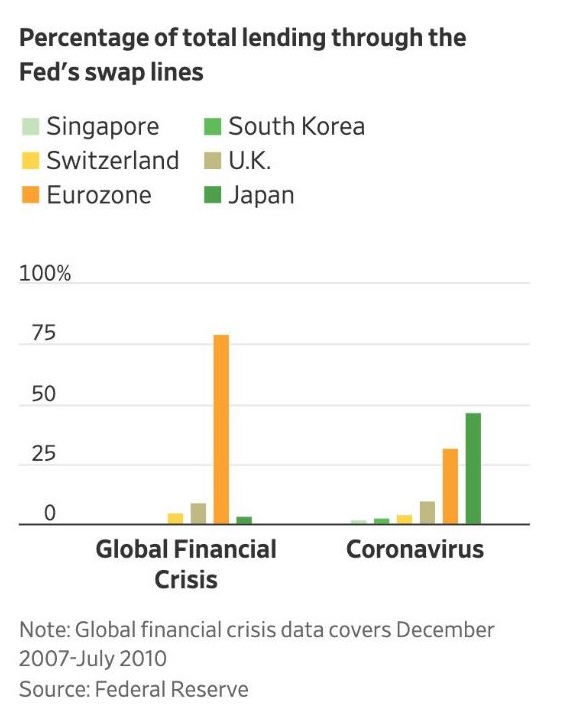

However, the Fed’s action cannot be ignored forever. It opened USD denominated swap lines in strong coordination with other central banks in the world. In the aftermath of the 2008 financial crisis, the swap lines were designed to help the Eurozone sovereign crisis – this time is Asia and emerging countries that need dollars to service debt.

{kind=link}

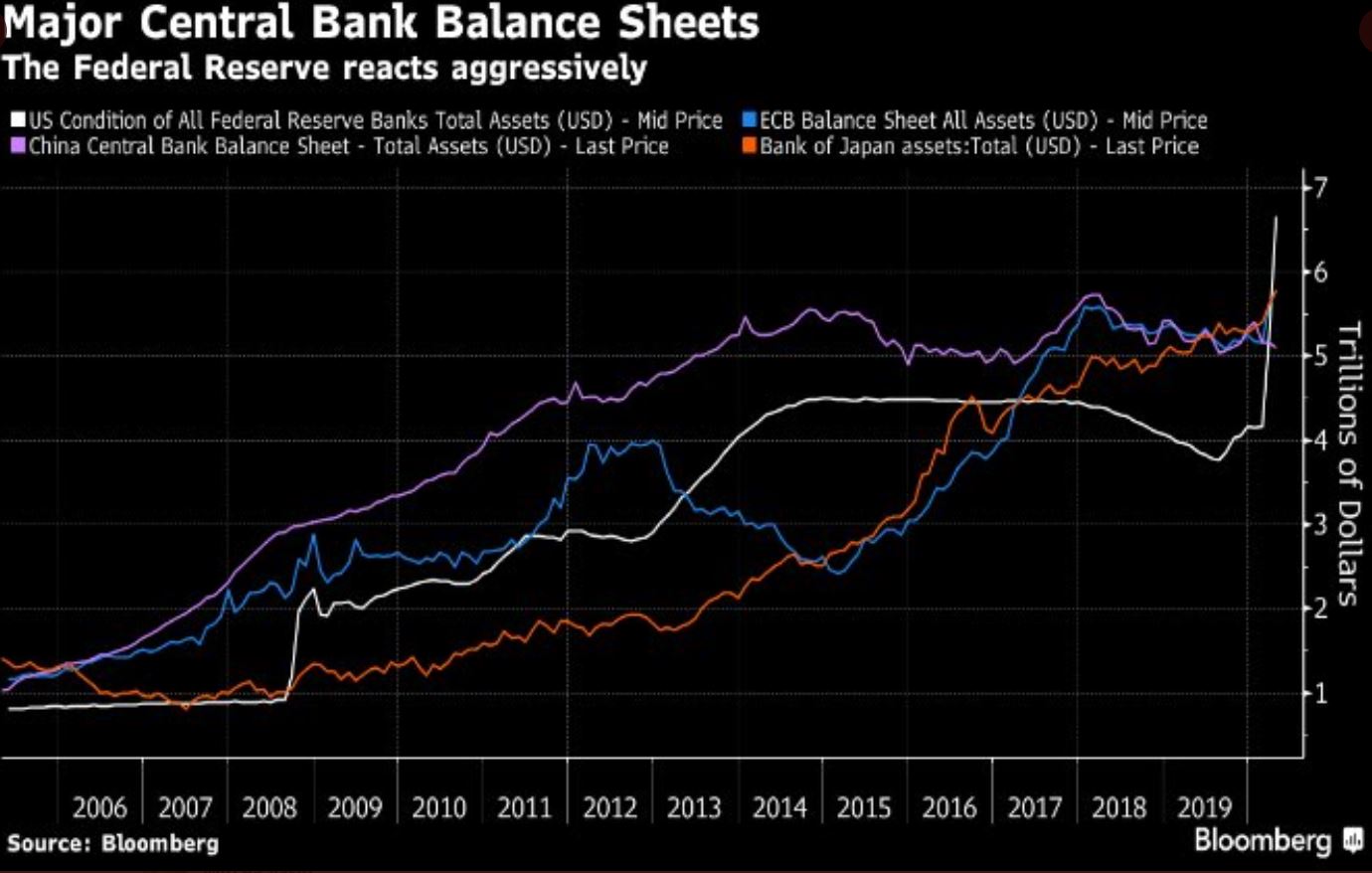

On top of that, the Fed restarted its quantitative easing program. A quick look at the major central banks’ balance sheet reveals the scale of the newly easing measures in the United States. The Fed’s easing pace quickly exceeded the one of its peers and rising.

{kind=link}

So why is the USD so strong again? A possible explanation is that the central banks’ actions take time to work through an economy. It takes several months to see the effect of a rate cut or hike, not to mention QE.

But that happens when economies function in normal conditions. In times of a health crisis, all economic principles mean nothing, and all that matters is the capital’s flight to safety.

For now, that safety has a name. The U.S. Dollar.