The Case for a Bullish EURUSD Scenario

The EURUSD consolidates for about two weeks now, after bouncing from the 1.08 area all the way to 1.14. Voices now call for a move back below 1.10, as the European Central Bank (ECB) signaled a massive demand for its TLTRO (Targeted Long-Term Refinancing Operations) – the banks in the Euro area took almost EUR1.4 trillion.

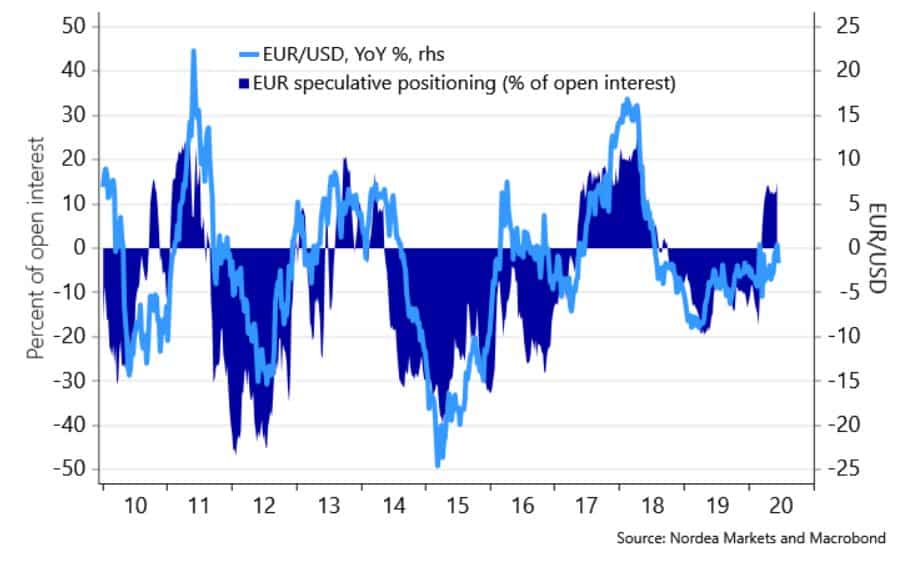

Naturally, all that money goes somewhere, and by flooding the market with newly printed Euros, the ECB creates the conditions for a weaker currency. However, a close look at the EUR speculative positioning (percentage of open interest), reveals that the market is about ten percent long the Euro against the USD – a lower exposure compared with previous data. In other words, there is more room to go.

{kind=link}

Since reaching the 1.14 level, the pair drifted lower in what seems to be a corrective pattern. It closed last week below the 1.12 level, with no important economic events scheduled this week.

But the focus these days is on how the market interprets the actions taken by the central banks. If the market sees the ECB as more proactive than the Fed, then the EURUSD pair has more room to go.

Moreover, uncertainty does not help the USD. With the US election just around the corner and record daily cases of new coronavirus infections, the United States does not offer the perfect investing scenario to grant appealing risk-reward ratios.

Finally, the US Treasury revealed that, while issuing more debt, it built a pile of cash (over $1.5 trillion) and stands ready to deploy it. In other words, the amount is roughly the equivalent of the ECB’s TLTRO injection, putting the Euro on equal foot with the USD, from a central banking point of view.

Further EURUSD strength is possible on a move above 1.14. Until then, the market may consolidate further, especially considering that summer trading conditions are already in place.