Analytical RBA Interest Rate Predictions in 2024 and Beyond

FXOpen

In an era of economic recalibration, the Reserve Bank of Australia's (RBA) interest rate decisions are in the spotlight. This FXOpen article delves into analytical predictions for RBA interest rates through 2024 and beyond, offering insights into the factors shaping Australia's monetary policy. The insights and forecasts that follow are aimed at helping traders, investors, and the public seeking to grasp the future of Australia’s economic landscape.

Current Australian Interest Rate Environment

At the time of writing, on the 19th of March, interest rates in 2024 in Australia stood at 4.35%, a decision orchestrated by the Reserve Bank of Australia. This rate, also known as the cash rate, is pivotal, influencing borrowing costs, the Australian dollar's value, and overall economic momentum.

This rate reflects a significant shift from the era of historically low rates seen between 2013 and mid-2022. The 2010s were a period of relative economic stability in Australia, with interest rates falling from 3% in 2013 to 0.75% at the end of 2019. As the COVID-19 pandemic set in, the RBA slashed rates further to support economic growth. By the end of 2021, rates fell to a record low of 0.1%.

As the pandemic's impact waned and Australia's economy embarked on a recovery path, the RBA initiated a series of rate increases to normalise economic conditions. This shift was evident as the cash rate climbed from 0.1% in May 2022 to 3.1% by the close of 2022, signalling a move to temper inflationary pressures without derailing economic recovery.

Inflation, indeed, has been a central concern for the RBA. Annual inflation rose sharply from 1.1% in Q1 of 2021 to a multi-decade high of 7.8% in Q4 2022. With the goal to steer inflation back to its target range of 2–3%, the central bank's strategy has been to manage inflationary pressures through rate adjustments. This strategy is taken through the lens of the RBA's commitment to economic stability, with a keen eye on both global economic trends and domestic demand and labour market conditions.

As of early 2024, the RBA's monetary policy stance remains cautious yet responsive. Despite easing cost pressures in Australia, inflation continues to hover above desired levels—at 4.1% per Q4 2023’s reading—prompting the RBA to maintain the cash rate at 4.35% at its most recent meeting in March 2024.

Interested in seeing how these dynamics affect Australian markets, like AUD/USD and the ASX 200? Head over to FXOpen’s free TickTrader platform to access real-time data and interactive charts.

Economic Analysis and Australian Interest Rate Forecasts from Leading Analysts for 2024

Analysts forecast the economic trajectory of Australia in 2024 to be a nuanced blend of initial restraint followed by a gradual relaxation of monetary policy. The first half of the year is expected to remain under the influence of the RBA’s existing monetary stance, with the cash rate held steady at 4.35%. This approach is indicative of the RBA's intent to carefully navigate between controlling inflation—which has been a persistent challenge—and not stifling economic growth.

Inflationary pressures, especially from the services sector, continue to be a significant concern for the RBA despite a faster-than-anticipated decrease in goods price inflation. The RBA forecast for trimmed mean inflation has been adjusted to 2.8% for the calendar year 2025, hinting at cautious optimism about achieving the inflation target. However, the services sector's resistance to price reductions underscores the complexities in the path to disinflation.

Domestically, several factors contribute to a restrained economic outlook for the early part of 2024. Consumer spending is forecasted to face challenges exacerbated by a fall in real household disposable income and a significant reduction in the household savings ratio to 1.1%. The sensitivity of the Australian economy to interest rate changes due to the prevalence of variable-rate mortgages amplifies the impact of the current monetary policy stance.

Moreover, the anticipated slowdown in population growth due to a decline in net overseas migration after a surge in 2023 is seen as likely to moderate one of the key growth drivers from the previous year. However, this does not alleviate the pressures on the housing market, characterised by low stock and high rental costs, which are expected to persist as significant economic constraints.

On the global front, Australia's economic outlook is further clouded by uncertainties, including potential geopolitical tensions and their impact on trade routes and energy prices. Specifically, any escalation in the Red Sea region could have broad implications for global trade and, by extension, the Australian economy. Additionally, the economic situation in China, particularly concerning its property sector and debt levels, poses indirect risks to Australia's economic stability.

Despite these challenges, the latter half of 2024 holds the potential for a more positive economic shift. The RBA's stance, as of February 2024, remains open to adjustments based on evolving economic data and risks. This flexibility suggests that monetary policy could lean towards easing should inflationary pressures subside as forecasted and economic conditions warrant. Tax cuts, real wage growth improvement, and an overall uplift in sentiment are expected to contribute to a recovery phase, enhancing domestic demand and potentially easing some pressures on household finances.

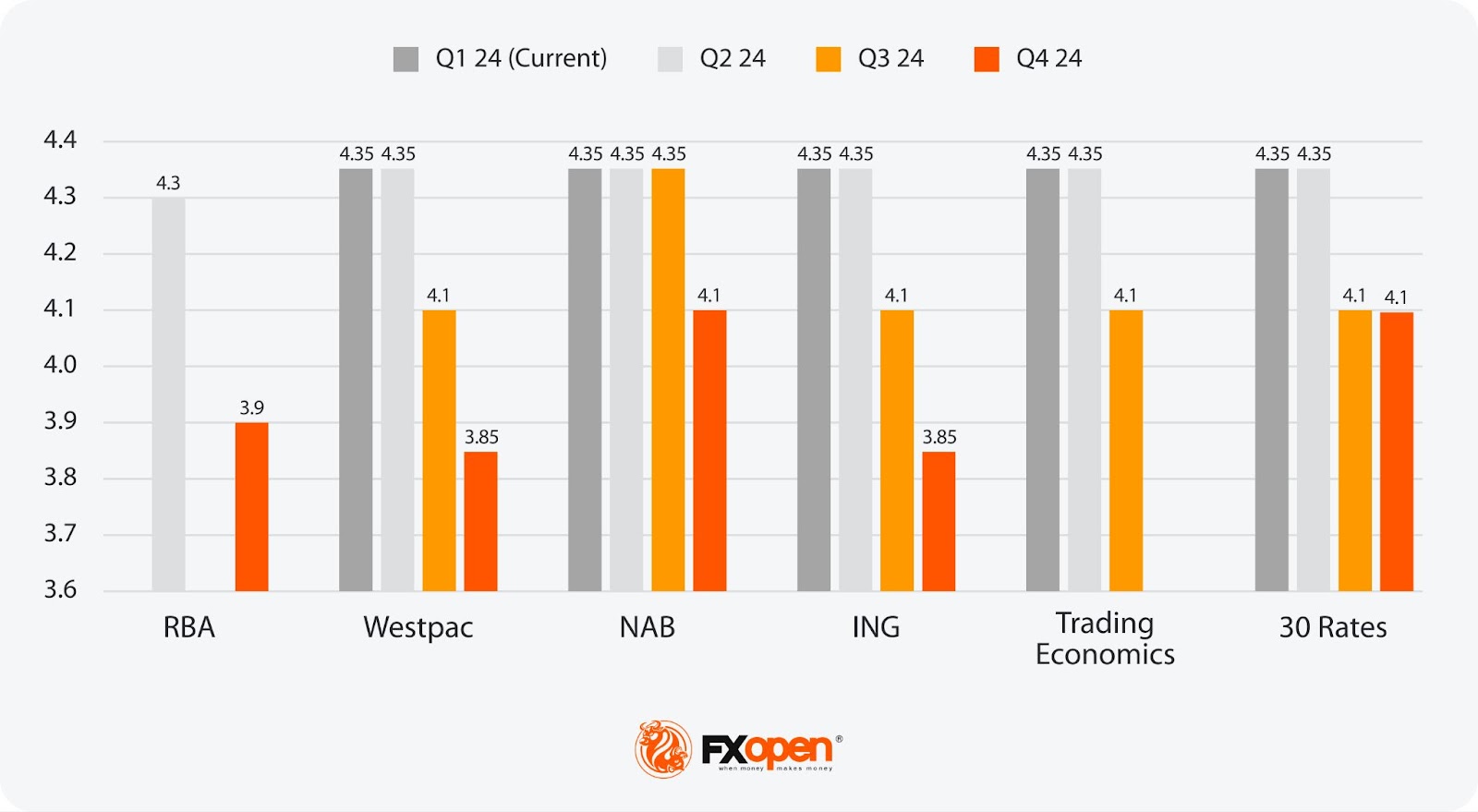

2024 Australian Interest Rate Predictions from Analysts

- Highest/Lowest Projection for Q2 2024: Consensus lies at 4.35%.

- Highest Projection for Q4 2024: NAB and 30 Rates both put Q4 Australian interest rates at 4.1%.

- Lowest Projection for Q4 2024: RBA, Westpac, and ING see rates declining to 3.85%.

Note: RBA projections are rounded to one decimal place.

Australian Interest Rate Forecasts in the Next 5 Years from Analysts

As we look towards interest rate predictions in the next 5 years in Australia, the RBA’s strategic focus on inflation control and economic stabilisation is expected to heavily influence their trajectory.

Looking to 2025, inflation is projected to align more precisely with the RBA's target range of 2-3%, with aspirations to reach the midpoint by 2026. This outlook hinges on an anticipated moderation in inflation, particularly noted in the quicker-than-expected decline in goods price inflation, despite services inflation maintaining a steadfast pace.

Given this backdrop, the period extending from 2025 onwards is set to be characterised by a cautious yet optimistic trajectory for interest rates. The RBA's monetary policy stance through the middle of 2024, which expects the cash rate to hover around its current level, serves as a precursor to potential easing as inflationary pressures wane. However, the path towards easing is complex, with several domestic and international variables at play.

Domestically, economic growth is forecasted to pick up from the latter part of 2024, carrying momentum into 2025. This resurgence is attributed to an expected relief in inflationary pressures and an improvement in household incomes, which could rejuvenate household consumption and, subsequently, economic growth.

Nonetheless, the labour market's dynamics, with nominal wage growth expected to stabilise, add layers to the interest rate discourse, emphasising the RBA's careful navigation between stimulating economic growth and maintaining inflation within target.

Internationally, the global economic landscape, particularly the synchronisation of monetary policies among advanced economies and geopolitical uncertainties, could influence Australia's economic prospects and, by extension, interest rate policies. The global economy's softer growth outlook may impact demand for Australian exports, thus affecting domestic economic conditions and the RBA's interest rate decisions.

Beyond 2025, interest rate predictions in Australia are influenced by the interplay between achieving sustainable economic growth and keeping inflation within the target range. The RBA's commitment to adjusting monetary policy in response to evolving economic indicators suggests a readiness to adapt to changing domestic and global economic conditions.

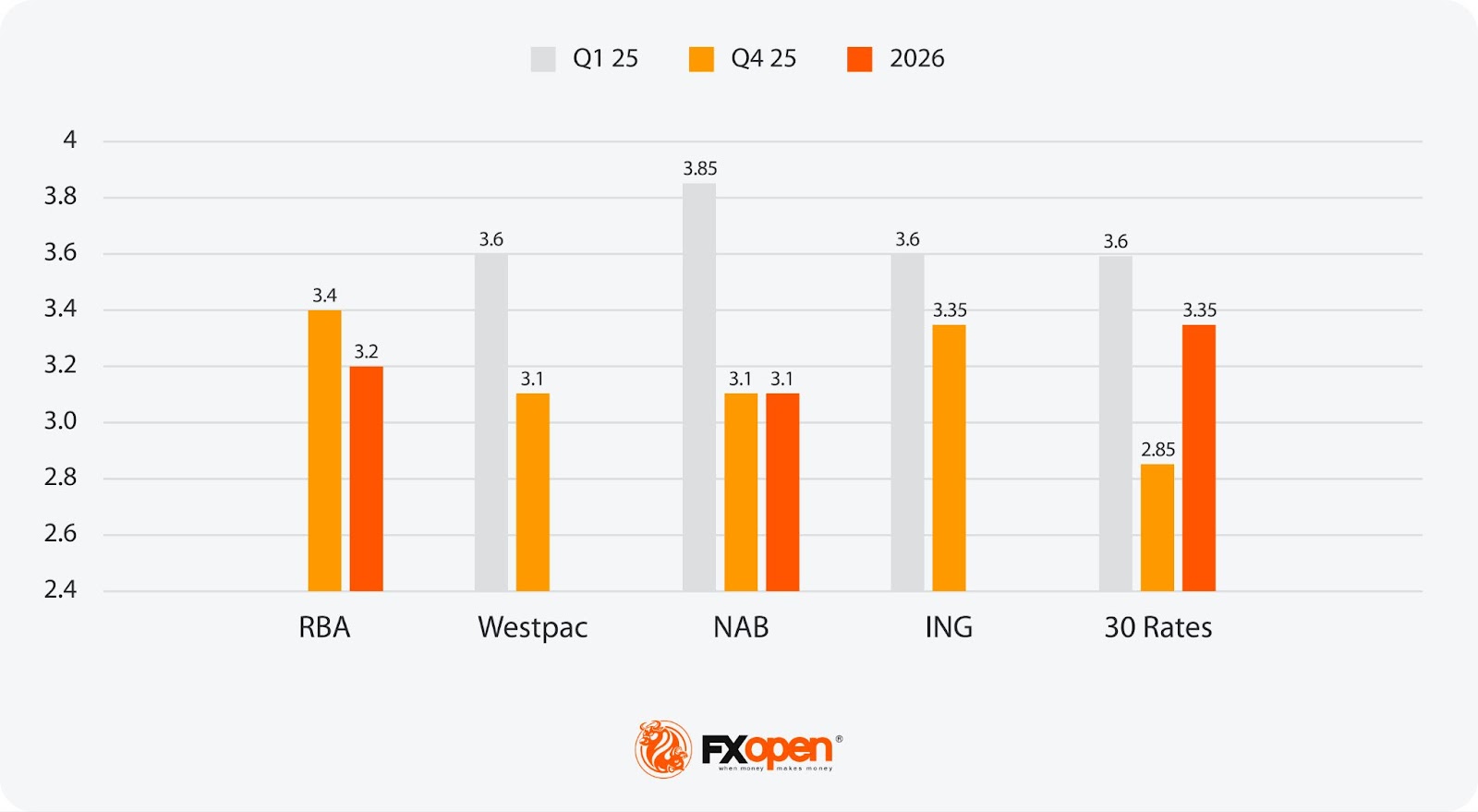

2025/2026 Australian Interest Rate Predictions

Q1 2025:

- Highest Projection for Q1 2025: NAB pegs Aussie rates at 3.85%.

- Lowest Projection for Q1 2025: Westpac, ING, and 30 Rates see rates falling to 3.60%

Q4 2025:

- Highest Projection for Q4 2025: RBA projects rates to stay relatively elevated at 3.4%.

- Lowest Projection for Q4 2025: 30 Rates anticipates a steep drop to 2.85%.

2026:

- Highest Projection for 2026: 30 Rates projects a rate hike from the end of 2025 to 3.35%.

- Lowest Projection for 2026: NAB puts 2026 Australian interest rates at 3.10%.

Note: RBA projections are rounded to one decimal place.

No predictions are available for 2027 onwards.

Factors Likely to Affect Future Australian Interest Rates

Australian interest rates are anticipated to be influenced by a myriad of factors in the coming years. The RBA will likely adjust its monetary policy in response to both domestic and global economic indicators to achieve its inflation and employment objectives. Key factors expected to impact Australian interest rates in the future include:

- Inflation Dynamics: Inflation is forecasted to move closer to the central bank's target range of 2-3% by 2025. The pace at which services and goods inflation moderates will be crucial in determining interest rate adjustments.

- Global Economic Conditions: Economic performance and monetary policy trends in major economies are projected to influence global demand for Australian exports, potentially affecting domestic interest rates.

- Domestic Economic Performance: Economic growth rates and consumer spending trends within Australia are expected to guide the RBA's policy stance, with efforts to stimulate or cool the economy as needed.

- Labour Market Conditions: Employment levels and wage growth are anticipated to influence domestic inflationary pressures, necessitating careful interest rate management by the RBA to maintain economic stability.

- Housing Market Developments: Given Australia's significant volume of variable-rate mortgages, the health of the housing market and lending practices are likely to have a direct impact on consumer spending and, consequently, interest rate decisions.

- External Shocks and Geopolitical Events: Unforeseen global events, including trade disputes and geopolitical tensions, are expected to pose risks to economic stability, potentially prompting the RBA to adjust interest rates in response.

The Bottom Line

Navigating the Australian economic landscape and interest rate environment from 2024 onwards presents a blend of cautious optimism and complex challenges. With the RBA's strategic focus aimed at inflation control and bolstering economic stability, the period up to 2029 hints at gradual adjustments rooted in evolving economic indicators.

For those keen on exploring opportunities in this dynamic environment, opening an FXOpen account offers a gateway to engaging with Australian financial markets, allowing traders to take advantage of anticipated shifts in Australian monetary policy via numerous assets, including currency pairs and indices, via CFD trading.

FAQs

How High Will Interest Rates Go in Australia?

Interest rates in Australia are expected to have peaked at the current rate of 4.35%. The Reserve Bank of Australia (RBA) has carefully navigated the economic landscape to manage inflation and support growth, with sources suggesting that the likelihood of further increases in the short term is low.

Will Interest Rates Keep Rising in Australia in 2024?

Interest rates are not anticipated to rise further in 2024. With the current rate considered to have reached its peak, the focus shifts towards maintaining economic stability and gradually adjusting policy as inflation aligns with target levels.

What Is the Interest Rate Forecast for the Next 5 Years in Australia?

Forecasts indicate a gradual decrease in interest rates from their current peak over the next two years. As inflationary pressures ease and the economy moves towards a more balanced growth trajectory, rates are expected to fall, reflecting the RBA's long-term monetary policy strategy. Longer-term projections aren’t currently available.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Stay ahead of the market!

Subscribe now to our mailing list and receive the latest market news and insights delivered directly to your inbox.

Latest articles

Gold: Attempt to Break Out of the Short-Term Trend

Fundamental backdrop

In April, US inflation stood at 3.8% year-on-year — the highest level since May 2023. A significant contribution came from rising fuel prices amid escalating tensions in the Middle East. Market reaction was somewhat paradoxical: instead of inflows

USD/JPY and USD/CAD Test Key Levels Ahead of the ADP Employment Report

The US dollar is holding on to its recently gained ground following a series of strong macroeconomic releases and a rise in US Treasury yields. Additional support for the greenback comes from resilient inflation readings, expectations that the Federal Reserve

EUR/GBP: June ECB Meeting Could Bring the Period of Equilibrium to an End

Fundamental backdrop

The divergence in the monetary policy paths of the ECB and the Bank of England is creating a mixed outlook for the pair. Having completed a cycle of eight consecutive rate cuts in 2025, the ECB left its